SO, THE DEAL HAS BEEN DONE and the new fisheries arrangement agreed. At the outset of the negotiations the UK government declared in The Future Relationship with the EU: The UK’s Approach to Negotiations (February 2020) that, “future fishing opportunities should be based on the principle of zonal attachment”.

As things have turned out, the new fisheries agreement has been designed (although nowhere in the agreement does it explicitly say this) to reduce the value of the fish landed by the EU fleet by the equivalent of 25% of the value it currently lands from the UK EEZ. To the extent that the new agreement is designed to reduce the share the EU lands from the UK EEZ it would be possible to argue that the deal is working towards zonal attachment but that it is only a quarter of the way there. What it delivers is historical share with a smidgeon of zonally attached adjustment. As to whether that is good enough is for the reader to judge.

It’s also a very back-to-front way of concocting a fisheries agreement.

Haggle over the money and then bodge the quotas to deliver whatever bargain was agreed. At the level of individual stock quotas there is not even a fig leaf of zonal attachment. It’s a fudge to deliver an agreed outcome. The following article will look at what the new fisheries agreement could have delivered, what is has actually delivered and whether or not it actually delivers what the politicians say it does.

The results

Before Tables 1 to 4 start to analyse what the deal delivers, the following paragraphs provide the reader with some notes about how the various figures have been arrived at. Our more impetuous and judgemental readers can, if they wish, skip the caveats and provisos and scroll straight forward to the tables, whilst those of you who always read the small print before signing on the dotted line are welcome to plough through these paragraphs in full.

• The tables summarize how the same selection of headline species or genera that featured in the previous articles will be impacted by the ‘deal’. This selection includes the main high-tonnage pelagics, fish supper favourites and a selection of gourmet’s delights; but it does not cover every species for which a TAC and quota are set. In order to help the general reader see the wood for the trees, species that are landed in smaller quantities or that are lower in value have been omitted from this selection.

• For the sake of simplicity and ease of presentation, each species is treated as a single stock, with a single TAC and a single UK or EU share. In reality both the old CFP and the ‘deal’ treat many species as a series of discrete stocks landed from specified fishing zones, each of which is allocated its own TAC and UK or EU shares. These have been aggregated by me for the purposes of the following tables to produce a single TAC and weighted average shares. So, for example, there are five separate Haddock stocks, seven separate Common Sole stocks and Annexes 1 and 2 of the ‘deal’ set shares for a total of 105 stocks. That’s why these tables were not produced the same day as the deal was announced. That might also tell you something about the level of scrutiny they may or may not have had.

• Although aggregating the separate stocks for a species substantially reduces the number of lines in the following tables, this approach does conceal one hidden danger. The TACs for the individual stocks can vary independently of each other and this means that, although the UK or EU shares for an individual stock do not change (leaving aside the adjustment period provided for by the ‘deal’), the weighted average shares for a species could.

• Although only the UK and the EU are parties to the ‘deal’, Annexe 2 does specify UK and EU, though not Norwegian, shares for stocks jointly managed with Norway. To the extent that this is the case, UK and EU landings from the Norwegian EEZ are included in the following tables.

• Landings from fishing zones not covered by Annexes 1 and 2 of the ‘deal’ have been excluded from the following tables.

• In all four tables, the 2020 TACs, as the most recent ones, are used to calculate current landings, whilst average shares for 2010-2016 (the period for which full figures were available in the EU database for its various national fleets) have been used to calculate the proportions of landings from the UK or EU EEZs, in line with the approach taken by previous articles in this series.

• The ‘deal’ provides for an adjustment period, running from 1st January 2021 to 30th June 2026 and during this period the UK and EU shares will change year by year until 2026. The ‘deal’ envisages that the shares arrived at in 2026 will then apply from 2027 onwards, with the first possible review four years after that. Since the intention of the ‘deal’ is that the position from 2026 should be the new norm, the following tables compare the current (2020) position with the 2026 position. The reader should remember that the 2026 position will not be achieved in one bound but through a series of annual steps, although for most stocks the largest change will occur between 2020 and 2021.

• What the deal actually specifies through its annexes are the UK and EU percentage shares of whatever TAC is set for a specified stock in a given year; but what the publicity surrounding the deal says it delivers is a 25% reduction by value of EU landings from the UK EEZ. This goal is never explicitly stated anywhere in the ‘deal’, even if this was the goal that informed the negotiations, and no tonnages or values are mentioned in the ‘deal’. The reader should bear in mind when reading this article and the ‘deal’ that it is the percentage shares – and nothing else – that have been agreed.

• However, in order to provide the general reader with a more easily comprehensible way of understanding the impact of the changes, the tonnages that might be landed in 2026 and the value of these landings have been calculated in various of the tables by applying the 2026 shares to the 2020 TACs and using average 2018 UK first sale prices (the values used in previous articles in the series) to calculate value. The reader should bear in mind that TACs and prices can go up and down and that individual TACs and fish prices can move independently of each other – one TAC or price might go up, whilst another might go down. Furthermore, fish prices can vary over the course of a year and can also differ from one market to another. In short, the projected 2026 tonnages and values will almost certainly never come to pass.

• For the same reason, whatever the publicists say, it is also impossible for the ‘deal’ to actually be certain of delivering a 25% reduction in the value of EU landings from the UK EEZ because it is difficult to forecast what TACs or prices might be five years hence. It can only say that this is what it would do if TACs and prices remained unchanged.

Having ploughed through the small print, what do the tables actually show?

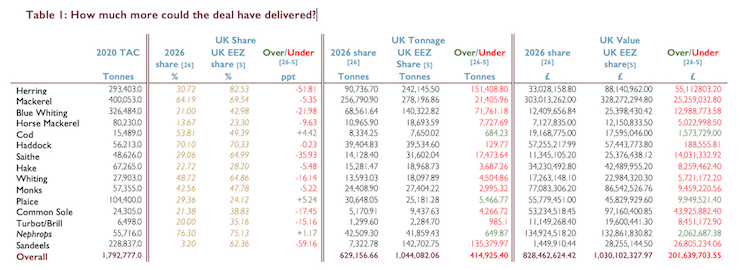

Table 1 looks at how much more the ‘deal’ would have delivered if it had been truly based on the principle of zonal attachment, i.e. the UK fleet is allocated the share landed from the UK EEZ.

The UK Share section compares 2026 share with share landed from the UK EEZ; with the final Over/Under column showing the percentage point difference between the share for the UK fleet and the share landed from the UK EEZ, that is the share the UK would land under full zonal attachment. Green figures are for species where the share allocated to the UK fleet exceeds the share taken from the UK EEZ, red figures are where UK fleet share is less than UK EEZ share.

The column is mainly red. There are only three species—Cod, Plaice and Nephrops where the UK 2026 share exceeds the share landed from the UK EEZ.

The UK Tonnage section applies the shares from the Share section to the 2020 TACs to project landings for 2026 and then calculates the difference between what the UK will be entitled to land 2026 and what it would have been entitled to land under full zonal attachment. Again, green figures indicate the ‘deal’ gives the UK more than zonal attachment, red less.

The UK Value section repeats UK Tonnage but in value terms. Once again, the overall figure is red but because some of the UK’s largest shortfalls are for relatively low value species (Herring, Blue Whiting, Sandeels) the relative shortfall (19.57%) is less than in tonnage terms (39.74%).

Overall, the current ‘deal’ entitles the UK to land some 400 kt or £200 million less than under full zonal attachment;

Table 2 looks at what the ‘deal’ actually delivered by comparing the proposed future UK shares with both current shares, as set by quota, and actual landings by the UK fleet, as calculated from average share of landings between 2010 and 2016, which may differ from the allocated share for various reasons.

In the first, Current, section, the shares allocated to the UK are compared with landings from the UK EEZ and the percentage point difference between Share20 and From UK EEZ, i.e. the difference between what the UK was allocated by the CFP and what was taken from its EEZ, is shown in the right-hand column. Positive figures in green are the percentage point increases that would occur if the UK share matched landings from its EEZ. Negative figures, in red. indicate the decreases that would occur if allocated share exceeded the share taken from the UK EEZ.

The column is entirely green, barring Plaice.

In the second section, the 2026 shares are compared with the current ones, i.e. official allocation against official allocation. The first column shows the percentage point increase in UK share by 2026, with figures in red indicating an increase that is less than the difference between landings from the UK EEZ and the current share, i.e. indicating an increase that is less than that required to achieve full zonal attachment, and figures in green indicating increases that are more than sufficient to achieve full zonal attachment. These percentage point increases are then translated into tonnage and value terms by applying the percentage point increase to the 2020 TAC, as already explained, and summed to produce overall totals.

The column is mainly, but not entirely, red. The only species for which the ‘deal’ exceeds zonal attachment are Cod, Plaice and Nephrops.

In the third section, the 2026 shares are compared not with current allocated share but with actual shares of landings by the UK fleet. The share a fleet lands may differ from the share it is allocated for a number of reasons, including various mechanisms for swapping or leasing quota. It has been argued that some of the gains in UK share delivered by the new UK shares specified by the ‘deal’ are illusory because they have, de facto, already been achieved in part by quota swaps or leasing. The left-hand column of this sections shows the percentage point difference between the share of actual landings and the 2026 share. Figures shown in red indicate a gain that is lower than the gain when current and 2026 allocated shares are compared (as in the previous section), green ones indicate gains that are greater than when comparing allocated shares. Whilst the column is fairly evenly split between red and green entries, the overall gain to the UK when comparing new allocated share with share of landings rather than current allocated share is clearly greater in both tonnage (94 kt v. 130.6 kt) and value (£124 m v. £158.6 m) terms.

Overall, comparing 2026 share with the UK’s actual share of landings rather than its allocated share results in greater gains for the UK than comparing allocated share with allocated share.

The claim made for the ‘deal’ is that it reduces EU landings from the UK EEZ by 25% when measured by value. Does it live up to even this modest claim? Your author’s task is not made any easier by the fact that neither the CFP nor the ‘deal’ actually specify EU landings from the UK EEZ. The only shares specified are for fishing zones that cut across EEZ boundaries. To solve this problem, Table 3 calculates the new EU share that would be the equivalent of a 25% reduction in EU landings from the UK EEZ for each species considered by this article and then compares this share with the 2026 share actually proposed by the ‘deal’.

How Table 3 works

The percentages the EU fleet lands from the UK and EU EEZs are calculated from landing records. The UK percentage is reduced by 25% and the adjusted UK and the EU percentages are then added back together to calculate the percentage of the current EU share that the new one would need to be to achieve a 25% reduction in EU landings from the UK EEZ. The current EU share is then multiplied by this percentage to yield the EU share [R] that would represent a 25% reduction in EU landings from the UK EEZ. The actual 2026 Share [26] proposed by the ‘deal’ is then subtracted from [R] in order to calculate the percentage point difference between the EU share that would actually represent a 25% reduction in landings from the UK EEZ and the 2026 share proposed by the ‘deal’. The Over/Under column lists these differences, with figures in red indicating the percentage point reduction that would be required to bring the 2026 share in line with the share that would be equivalent to a 25% reduction and green figures indicating the percentage point increase that would be required.

Although one or two of the proposed 2026 shares are close to the figure required to achieve the 25% reduction, none hit the bull’s eye and several (Herring, Blue Whiting, Cod, Sandeels) are more than a few percentage points wide of the mark. Why, one might ask, do these proposed 2026 shares exhibit such a wide scatter about the target? As well as the deal as a whole being designed in a back to front sort of a way, has it been compounded by a bit of good old-fashioned horse trading? So much for the sacred principle of zonal attachment.

However, the claim made for the ‘deal’ is an overall 25% reduction not that each species is reduced by 25% and that the reduction is measured by value not tonnage. Since each of these species differs in value and is landed in different quantities it is not possible to calculate from Table 3 whether or not the ‘deal’ delivers on what is claimed for it.

To see whether the ‘deal’ delivers on its claim, proceed to Table 4.

In Table 4 the EU quotas in 2020 and 2026 are calculated by applying the relevant EU shares to the 2020 TACs, and the reductions in landings are then calculated by subtracting the 2026 figures from the 2020 ones. EU landings from the UK are calculated by applying the historical share of EU landings taken from the UK EEZ to EU landings and the percentages of EU landings from the UK EEZ that these reductions represent are then calculated.

The percentage reduction for each species is shown in the right-hand column, with percentages below 25% shown in red and those above in green. However, the ‘deal’ does not claim that landings are reduced by 25% for each species but for overall landings. What’s more the tonnages landed for each species differ, as do their values. In order therefore to determine whether the ‘deal’ has delivered on its claim to reduce the overall value landed by the EU from the UK EEZ by 25%, the reductions in values for the individual species are totalled and the percentage that this represents of overall EU landings from the UK EEZ calculated.

For the 15 species being considered here, that reduction is 25.52%. In other words, at least for these 15 species, the ‘deal’ has delivered.

Some words of caution

The calculated reduction in value is based on the assumption that the TACs and values do not alter between now and 2026 but this is highly unlikely to be the case. So, in short, although the projected reduction in value five years hence using the proposed new shares and based on current TACs and values would match the target of 25%, the actual reduction in five years’ time is highly likely to be something different, maybe more, maybe less.

Furthermore, the projected reduction is highly dependent upon how TACs and values shift for a few key species. The reduction for Mackerel, for example, is both well above the target 25% and is tonnage terms the highest for all the species. Mackerel is a species for which TACs have recently been cut. Future cuts – or increases – could have a significant impact on the relative cut in EU landings.

Finally, the target for the reduction in EU landings is equivalent to 25% of the value of EU landings from the UK EEZ but the shares used to deliver this – both the current ones and the 2026 ones – apply across entire fishing zones and do not simply apply to the UK EEZ. It would be perfectly possible for EU fleets to continue to fish in the UK EEZ to an undiminished extent and for all the reduction to be achieved through reduced fishing in the EU EEZ and for the target set for the ‘deal’ still to be achieved.

Summary

Assuming unchanged TACs and prices, for the 15 species considered by this article, the ‘deal’ delivers a reduction in EU landings and a transfer to the UK that is the equivalent of 25.52% by value of EU landings from the UK when comparing allocated share with allocated share.

For the 15 species considered by this article, this reduction of EU share and transfer to the UK amounts to 93,961.66 tonnesand is worth £124,005,159.62. When all the other species subject to quota not considered by this article are taken into account it seems likely that the deal does deliver a 25% reduction in EU landings from the UK EEZ worth in the region of £145 million, as has been claimed for the ‘deal’.

However, for the 15 species considered by this article, there are a further 414,925.40 tonnes worth £201,639,703.55 that the UK could have secured if its future share were truly based on zonal attachment, as the government stated was its intention at the outset of the negotiations.

Given the fact that the ‘deal’ has recovered substantially less than half the net tonnage and value that the EU currently lands from the UK EEZ, following articles in this series will examine ways in which the UK might work to secure further transfers of share from the EU to the UK.

After a first degree in zoology followed by research in developmental genetics, Neil Stratton worked for a number of European publishers before beginning an analysis of European fish landings with the think tank EH99 in the spring of 2018. The recently published report Fair Shares for All is based on this analysis.

Image of Atlantic Cod by VIVIANE MONCONDUIT from Pixabay